The Federal Board of Revenue (FBR) recently executed a direct FBR tax recovery of Rs. 30 million from a citizen’s bank account. This strategic move followed an investigation into alleged residency misrepresentation and the submission of forged appellate documents. Consequently, the FBR utilized Section 140 of the Income Tax Ordinance to secure state revenue after the taxpayer failed to provide evidence for claimed exemptions.

The Structural Mechanics of FBR Tax Recovery

The FBR identified a discrepancy in the taxpayer’s status. Although the individual publicly portrayed himself as a non-resident expat, he declared himself a resident in his 2017 and 2018 tax returns. This distinction is critical because residents remain liable for tax on their worldwide income. Furthermore, the individual claimed exemptions on Rs. 23.52 million in foreign income, which significantly exceeded the legal limit of Rs. 5 million.

Legal Framework and Compliance Calibrations

The department followed a precise legal sequence before initiating the FBR tax recovery. Specifically, the FBR issued notices under Section 122(9) and provided multiple opportunities for the citizen to furnish documentary evidence. When no evidence was provided, the FBR amended the tax assessment. Consequently, a formal tax demand of Rs. 30 million was raised. When the amount remained unpaid, the FBR exercised its power under Section 140 to recover the funds directly from the bank.

- Section 82: Defines residency based on a 183-day stay in Pakistan.

- Section 137 & 138: Governs the timing of tax payments and formal recovery notices.

- Section 140: Empowers the FBR to direct banks to transfer funds for unpaid liabilities.

The Situation Room Analysis

The Translation

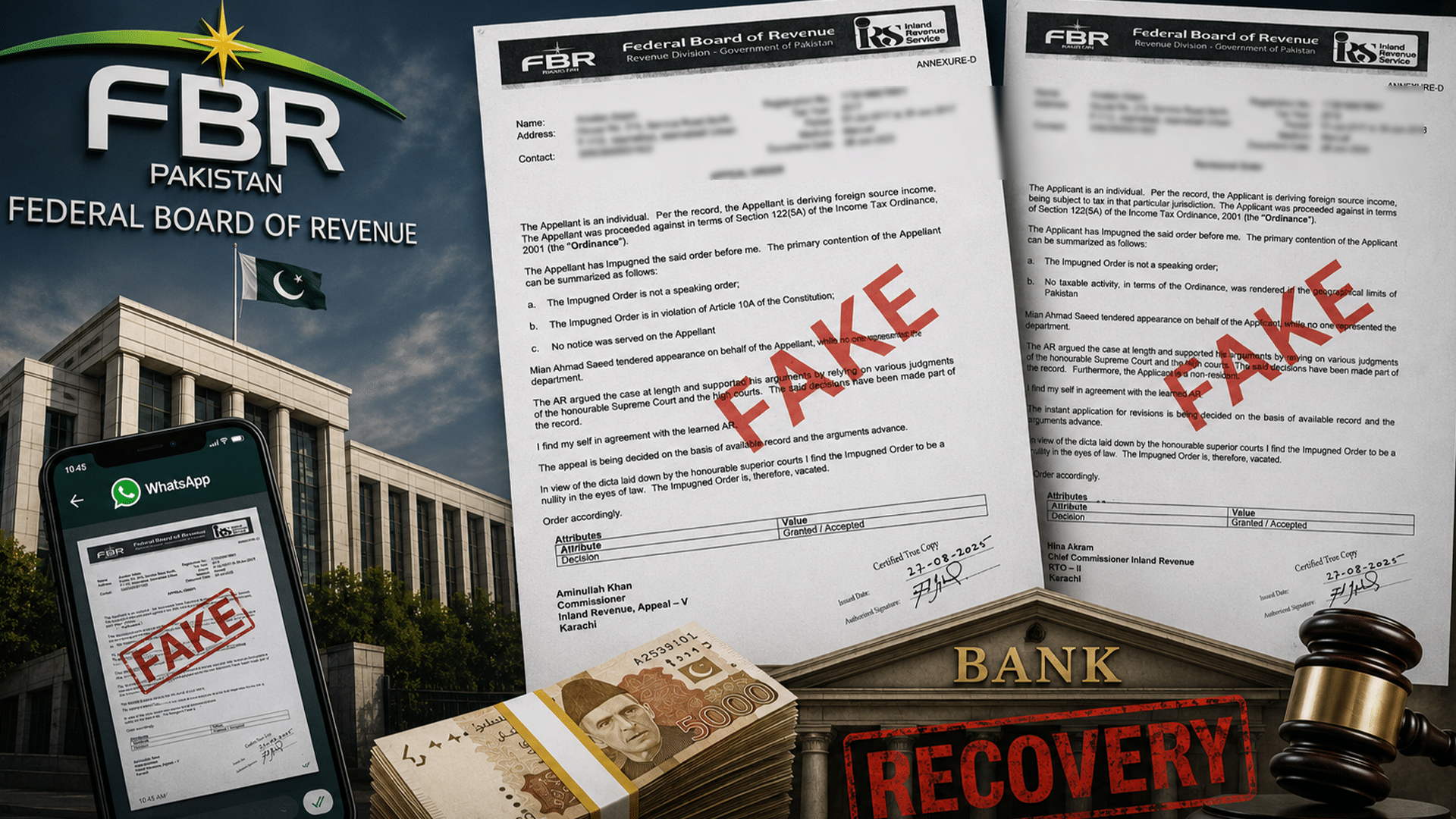

In simple terms, the FBR is moving away from passive observation toward active enforcement. The “183-day rule” is the baseline for residency. If you stay in Pakistan for more than half a year, your global income is taxable here. The FBR viewed the taxpayer’s attempt to use WhatsApp-shared “fake” documents as a systemic threat, necessitating a decisive structural response to maintain the integrity of the Inland Revenue System (IRS).

The Socio-Economic Impact

For the average Pakistani citizen, this case highlights the necessity of precise record-keeping. As the FBR digitizes its processes, the ability to track discrepancies between public personas and legal filings increases. For professionals and students, this ensures a more transparent system where the tax burden is distributed based on actual residency and documented income. Consequently, this precision reduces the fiscal gap that often plagues national development projects.

The Forward Path

This development represents a Momentum Shift. The FBR’s willingness to execute direct bank recoveries signals a transition into a more disciplined fiscal environment. While the sharing of private details on social media remains a point of contention, the legal enforcement of Section 140 demonstrates that the state is calibrating its tools for maximum efficiency. This move sets a new baseline for tax compliance in Pakistan.