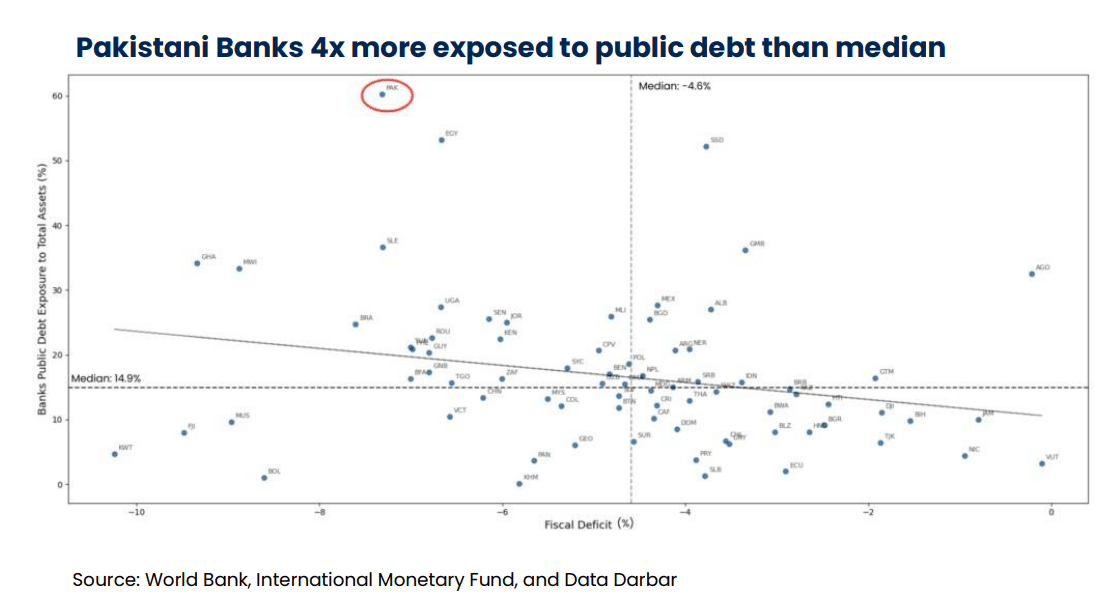

Pakistan’s financial architecture is facing a calibrated but concerning shift as domestic banks become the primary creditors to the state. A recent policy brief reveals that government debt exposure in Pakistani banks has reached 60% of total assets. This figure is four times the global median of 14.9% and represents the highest ratio among 80 countries surveyed. Consequently, the banking sector has transitioned from a facilitator of private commerce to a structural financier for Islamabad’s fiscal deficits.

Structural Imbalance: The Global Government Debt Exposure Baseline

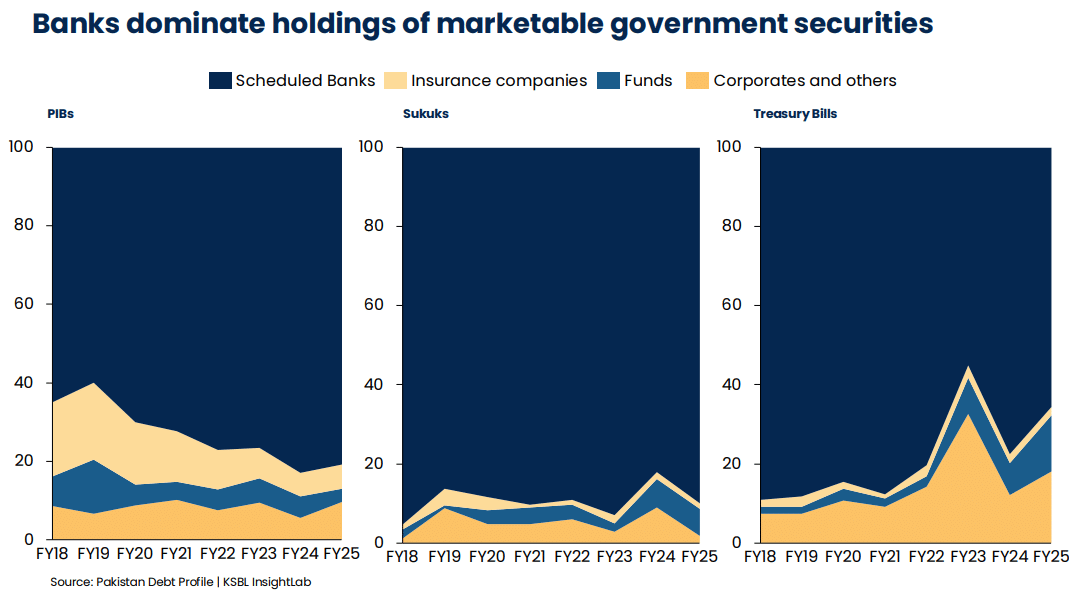

The Karachi School of Business and Leadership (KSBL) highlights a deepening financial dependency between the state and the banking sector. Public debt surged from Rs. 19.7 trillion in 2016 to an estimated Rs. 80.5 trillion by fiscal year 2025. Strategically, banks have absorbed much of this growth, with domestic government debt holdings currently reaching Rs. 54.5 trillion. Scheduled banks now hold approximately 79% of all marketable government securities, totaling Rs. 36.8 trillion.

The Precision Paradox: Why Banks Choose Sovereign Debt

The attraction to government securities is mathematically straightforward for financial institutions. These assets offer high returns with a zero-risk weighting under current regulatory frameworks. Furthermore, they require minimal underwriting compared to private sector loans. In contrast, lending to businesses consumes capital and exposes banks to default risks. Small and medium enterprises (SMEs) are often ignored due to thin credit histories and weak documentation.

As a result, Pakistan’s private sector credit stands at a meager 11.5% of GDP. This baseline is significantly lower than regional peers like India and Bangladesh. Small businesses receive less than 10% of total private credit, despite their role as a catalyst for employment. The massive government debt exposure has effectively crowded out the capital needed for entrepreneurial innovation.

The Situation Room Analysis

The Translation (Clear Context)

In simple terms, banks have stopped acting as engines for business growth and have instead become high-interest savings accounts for the government. Because the state is a “guaranteed payer,” banks have no incentive to take risks on local startups or factories. This creates a feedback loop where the government borrows to pay off previous debts, and banks profit without actually investing in the productive economy.

The Socio-Economic Impact

This structural shift directly hampers the daily life of Pakistani citizens. For the aspiring entrepreneur in Lahore or the small-scale farmer in Sindh, bank loans are nearly impossible to secure. When 60% of a bank’s money is tied up with the state, there is less liquidity for home loans, car financing, or business expansion. This stagnation limits job creation and keeps the middle class trapped in a high-inflation, low-growth environment.

The Forward Path (Opinion)

This development represents a Stabilization Move that has morphed into a structural bottleneck. While it keeps the government solvent in the short term, it paralyzes long-term national advancement. We must implement a calibrated policy shift that penalizes excessive sovereign exposure and incentivizes private sector lending. Without this pivot, the banking sector will remain a tax-harvesting tool rather than a catalyst for the next generation of Pakistani innovators.