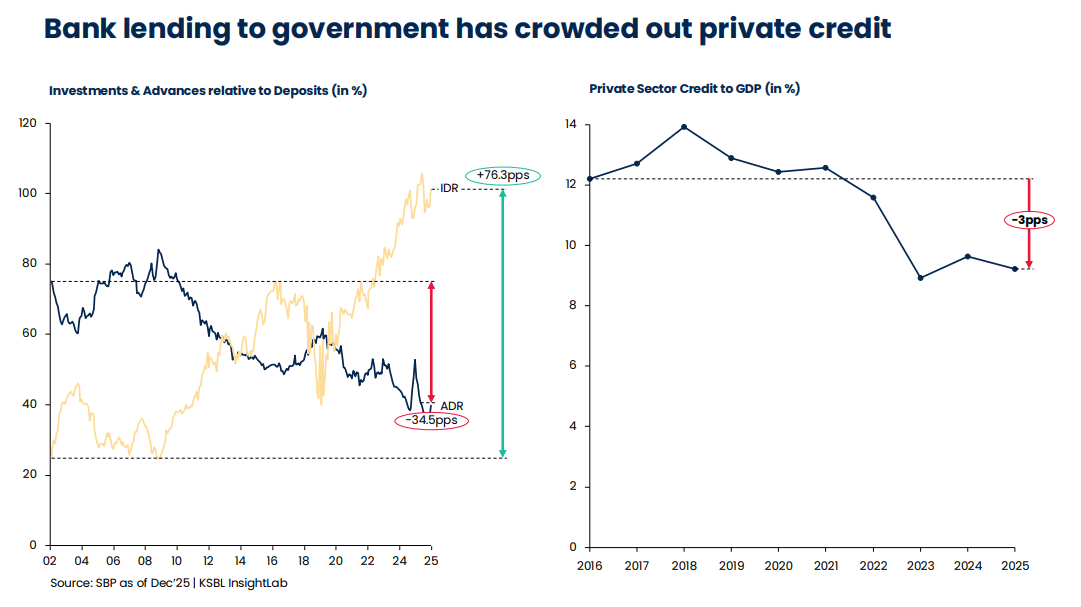

The structural health of an economy depends on capital velocity, yet Pakistan’s current financial architecture is prioritizing sovereign debt over Private Sector Lending. Recent data reveals that the government’s attempt to force banks toward small business financing through tax penalties has largely failed. Consequently, banks are choosing to absorb higher tax rates rather than expanding credit to riskier borrowers.

The Failure of ADR-Linked Tax Penalties

For years, policymakers calibrated specific measures to discourage banks from parking funds in government securities. To trigger a shift, the government introduced tiered taxation for banks with an Advances to Deposits Ratio (ADR) below 50 percent. However, the banking industry showed significant resistance to this structural nudge.

Specifically, a policy brief from the Karachi School of Business and Leadership (KSBL) indicates that the strategy yielded minimal results. Instead of increasing loans, banks accepted a higher flat tax rate of 44 percent. This choice proves that financial institutions view the risk of Private Sector Lending as more costly than the burden of aggressive taxation.

Why Banks Prioritize Government Securities Over Risk

Lending to local businesses requires intensive underwriting and consumes significant regulatory capital. In contrast, government securities like Treasury bills and Pakistan Investment Bonds offer a zero-risk weighting. These instruments provide attractive returns with minimal administrative effort, creating a catalyst for banks to avoid the complexities of SME financing.

Furthermore, SMEs often operate with limited documentation and weak collateral. Consequently, banks perceive these entities as high-risk prospects. With ADR levels currently hovering below 40 percent, access to credit remains a significant barrier for the 90 percent of businesses that drive Pakistan’s industrial baseline.

:max_bytes(150000):strip_icc()/Financial-inclusion_final-9c5b63eb93b54e55aa4b4c9df26788de.png)

The Situation Room Analysis

The Translation (Clear Context)

The government tried to use “tax bullying” to make banks lend to the public. By taxing banks more if they didn’t lend out at least half of their deposits (the ADR ratio), the state hoped to spark economic activity. Instead, banks calculated that it is cheaper to pay a 55% effective tax rate than to risk losing money on loans to businesses that might default. This highlights a fundamental lack of trust in the legal and recovery systems of the country.

The Socio-Economic Impact

For the average Pakistani entrepreneur or graduate, this means the “Credit Ceiling” remains unbreakable. When banks refuse to fund Private Sector Lending, startups cannot scale, and small shops cannot modernize. This stagnation forces the youth to seek opportunities abroad or remain trapped in low-productivity sectors. Essentially, the banks are funding the government’s deficit while the citizens’ innovative potential remains underfunded.

The Forward Path (Opinion)

This development represents a Stabilization Move that has reached its limit. While high taxes help the government recover short-term revenue, they do not build a sustainable economy. To achieve a “Momentum Shift,” Pakistan must reform its collateral laws and documentation standards. Until the “cost of risk” is lower than the “cost of tax,” banks will continue to act as safe-deposit boxes for the state rather than engines for the people.