Macroeconomic stability requires a calibrated approach to monetary policy, and the recent shift in the Karachi Interbank Offered Rate (KIBOR) indicates a structural recalibration. Market participants observe as borrowing costs fall across major maturities following the State Bank of Pakistan’s (SBP) decision to maintain the policy rate. This movement suggests a growing confidence that regional stability and strategic mediation will successfully drive inflation toward the target 5-7% range.

Why Borrowing Costs Fall Under Current SBP Strategy

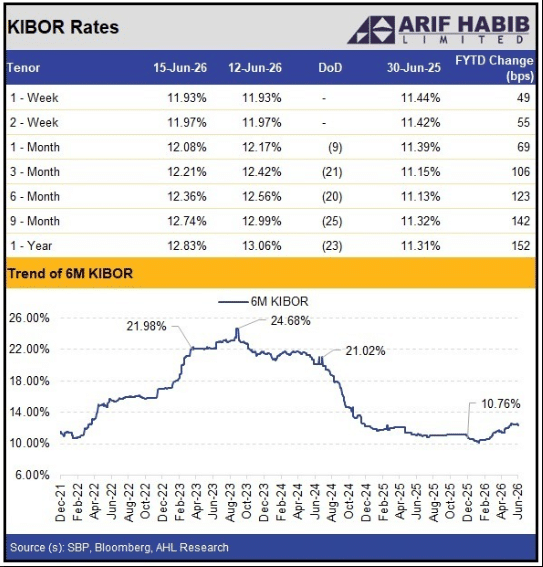

Data from Arif Habib Ltd confirms a downward trajectory across the yield curve. While short-term tenors such as the one-week and two-week KIBOR remained steady at 11.93% and 11.97% respectively, longer-dated papers showed significant easing. Specifically, the six-month rate dropped by 20 basis points to 12.36%, while the one-year tenor eased by 23 basis points to 12.83%. Consequently, these adjustments reflect a market that is actively pricing in softer global oil prices and the benefits of the recent US-Iran ceasefire.

Detailed KIBOR Adjustments

- One-Month Rate: 12.08% (-9bps)

- Three-Month Rate: 12.21% (-21bps)

- Nine-Month Rate: 12.74% (-25bps)

- One-Year Rate: 12.83% (-23bps)

The Translation: Deciphering the Market Signal

In “Next Gen” terms, the decline in KIBOR represents the market’s “vote of confidence” in future price stability. When the SBP holds rates steady despite previous pressures, it signals that the peak of the interest rate cycle has likely passed. Banks are now lending to each other at lower rates because they expect the cost of money to decrease as inflation stays within a manageable single-digit corridor. This creates a catalyst for cheaper commercial credit and improved liquidity within the financial system.

Socio-Economic Impact: What This Means for You

For the average Pakistani citizen, these falling rates serve as a baseline for improved purchasing power. Lower KIBOR rates eventually lead to reduced markups on consumer products, including auto loans and home financing. Furthermore, for small-to-medium enterprises (SMEs) in urban centers like Karachi and Lahore, lower borrowing costs mean more capital for expansion and job creation. Conversely, in rural areas, reduced energy-linked production costs—driven by the same global factors easing inflation—can help stabilize the price of essential commodities.

The Forward Path: Architect’s Perspective

This development represents a Momentum Shift. While KIBOR rates remain higher than their June 2025 levels, the current trajectory suggests that the economy is moving toward a more sustainable equilibrium. If energy prices remain low and regional geopolitical tensions continue to de-escalate, we expect a further easing of domestic cost pressures. This is not merely a stabilization move; it is the precision engineering of a more resilient financial landscape for Pakistan’s next generation.