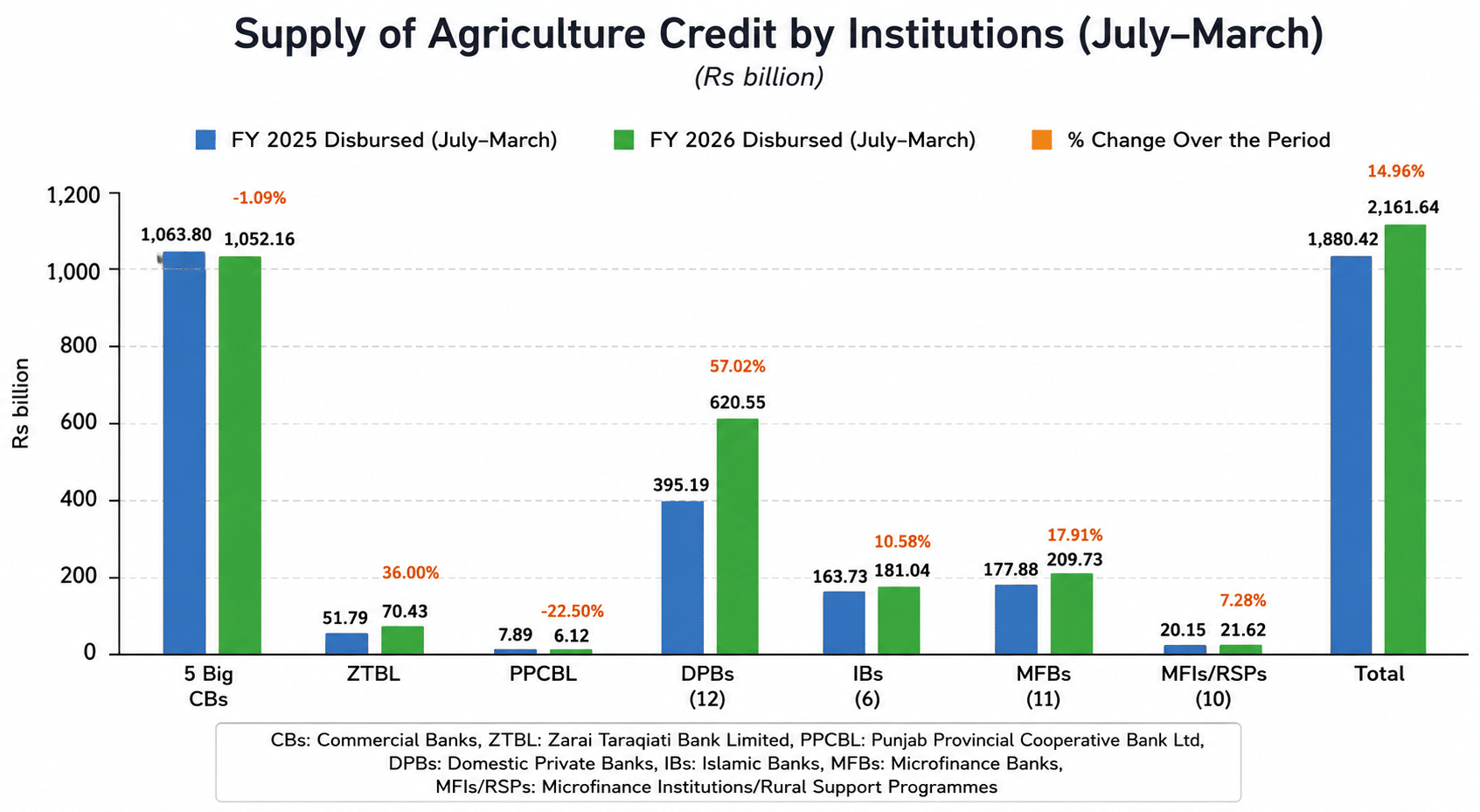

Pakistan’s agricultural credit growth signifies a calibrated shift toward a more robust, capital-intensive farming ecosystem. Total disbursements reached Rs. 2.16 trillion during the first nine months of FY26. Consequently, this represents a significant 15 percent increase compared to the previous fiscal year. Financial institutions are now aligning their credit facilities with the evolving needs of the domestic agribusiness landscape. This structural expansion serves as a vital catalyst for national food security and systemic economic efficiency.

What This Means for Our Digital Frontier

The Translation: Deciphering the Fiscal Surge

In technical terms, the banking sector has transitioned from passive lending to active market participation. Five major commercial banks spearheaded this movement by disbursing Rs. 1.05 trillion. Meanwhile, Islamic banks and microfinance institutions provided essential liquidity to underserved niches. The data indicates that 70.6 percent of the annual target of Rs. 3.06 trillion is already met. This suggests a higher baseline for institutional trust in the agricultural sector’s ROI (Return on Investment).

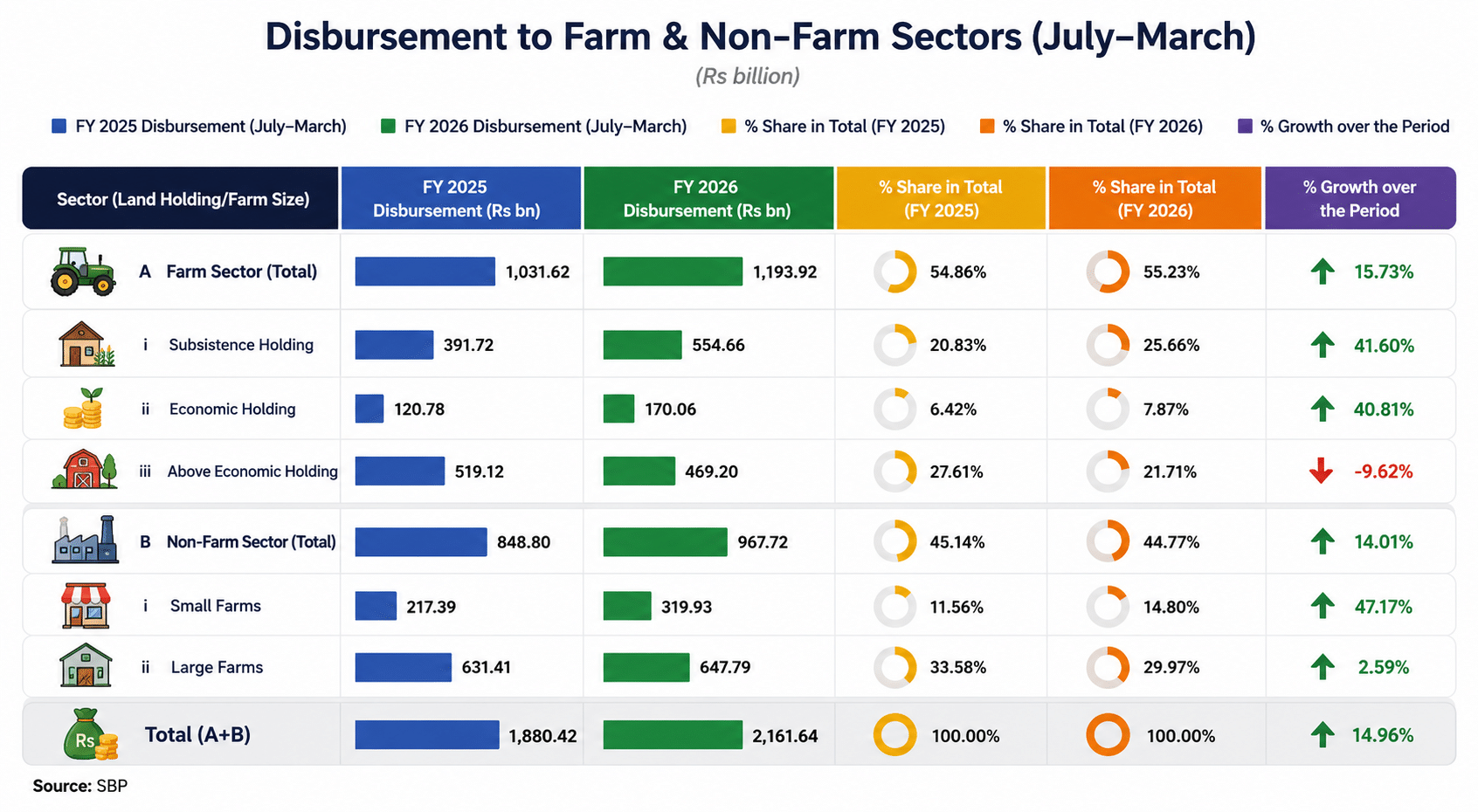

Precision lending is also evident in the sub-sector allocation. Farm sector financing dominated the landscape, absorbing Rs. 1.19 trillion. Specifically, credit to subsistence farmers surged by 41.6 percent. This jump indicates that formal financial channels are finally penetrating the traditional agrarian barriers. Furthermore, development loans increased by 22.6 percent, highlighting a strategic investment in farm machinery and productivity-enhancing infrastructure.

Socio-Economic Impact: Precision Lending for Rural Prosperity

For the average Pakistani citizen, this surge in agricultural credit growth directly impacts the cost of living and food availability. Higher credit access allows farmers to purchase certified seeds and optimized fertilizers. Consequently, this stabilizes crop yields and prevents drastic price fluctuations in urban markets. Students and young professionals in rural areas also benefit as agribusinesses modernize, creating high-skill employment opportunities within the livestock and digital farming sectors.

The introduction of the ZarKhez e ecosystem is a pivotal milestone. This technology-enabled platform uses alternative data sources for risk assessment. By automating these processes, the State Bank of Pakistan (SBP) reduces the friction traditionally faced by small-scale borrowers. This systemic efficiency ensures that capital reaches the most productive segments of the economy without bureaucratic lag.

The Forward Path: Momentum Shift or Maintenance?

This development represents a definitive Momentum Shift. The transition from manual land record verification to digital ecosystems like ZarKhez e marks a structural evolution in Pakistan’s financial architecture. However, to maintain this trajectory, the government must ensure the Risk Coverage Scheme for Small Farmers remains fully funded. Expanding the Electronic Warehouse Receipt Financing will also be critical. If we continue this trajectory, Pakistan can move from a subsistence-based model to a surplus-driven agricultural powerhouse by FY2028.