The escalating geopolitical landscape in the Middle East has profoundly impacted global energy security, creating an urgent imperative for system resilience. Specifically, disruptions to shipping via the Strait of Hormuz, a critical conduit for nearly 20% of global oil and gas, highlight the strategic value of Middle East oil pipelines as crucial alternative export routes. While these pipeline networks cannot fully replicate Hormuz’s capacity, their calibrated expansion and optimized utilization are vital for stabilizing international energy supply chains and mitigating significant economic pressures.

The Strait of Hormuz: Calibrating Global Energy Flow

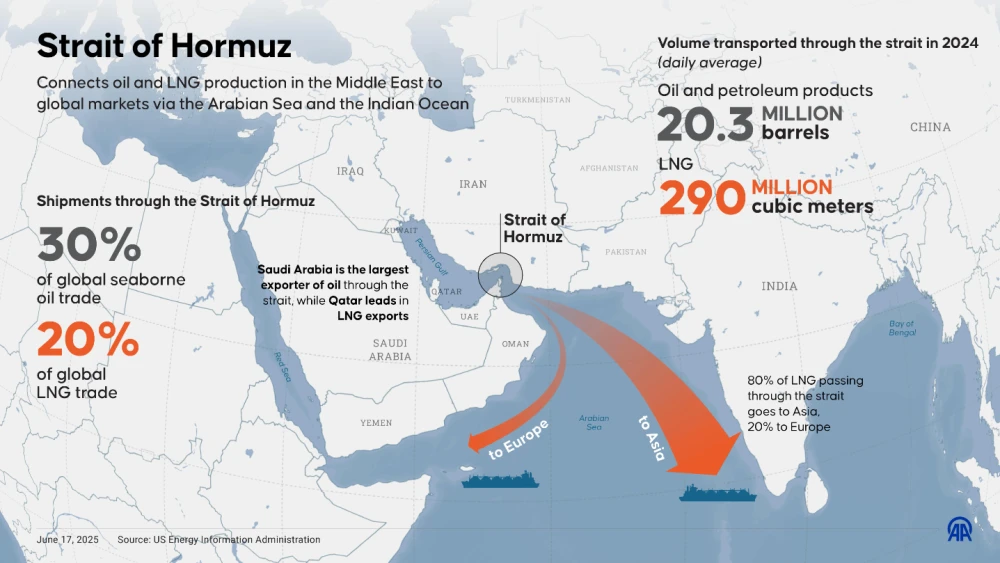

The United States–Israel conflict with Iran, now in its fourth week, has directly introduced severe disruptions in maritime traffic through the Strait of Hormuz. This narrow waterway, historically responsible for transporting approximately 20 million barrels of oil and gas daily, is central to connecting Gulf producers with global markets. Consequently, these escalations have placed immense pressure on international energy sectors, necessitating immediate adaptive strategies.

Following military actions in early March, a senior adviser to the Islamic Revolutionary Guard Corps declared the Strait effectively closed. Although Iran later clarified that passage was not entirely blocked, vessels now require Tehran’s explicit approval to transit. This strategic shift has drastically reduced shipping activity by over 95%, stranding around 2,000 vessels. Notably, some tankers from India, Pakistan, and China have reportedly gained permission to proceed, showcasing a calibrated approach to selective transit.

Strategic Pipeline Alternatives: Enhancing Middle East Oil Pipelines Capacity

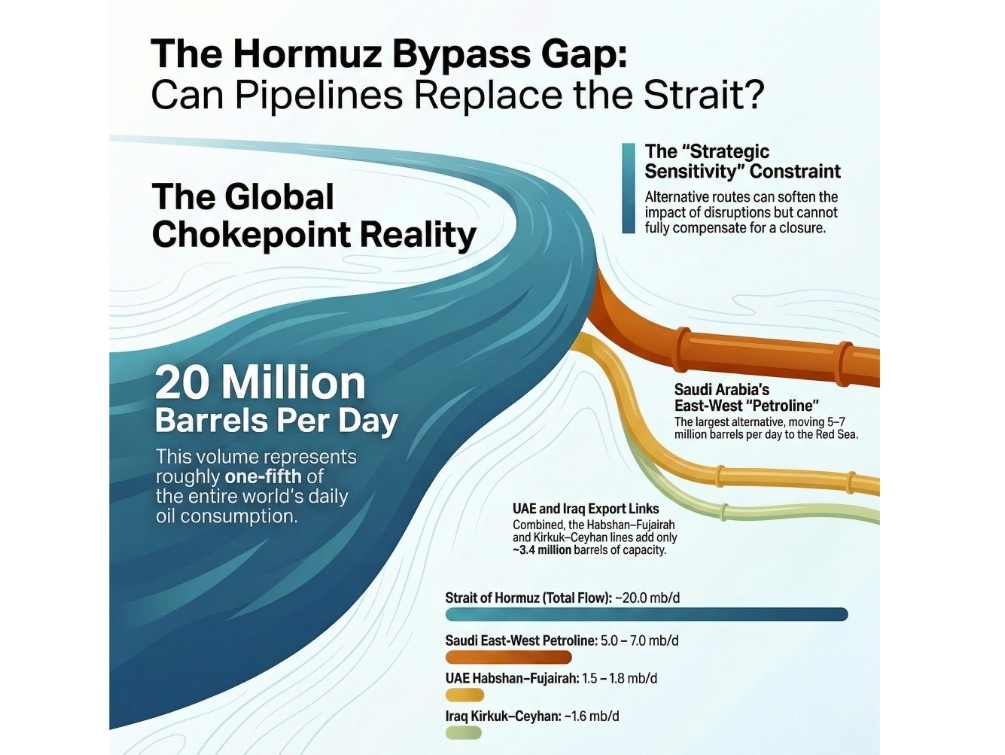

With critical maritime routes facing unprecedented disruption, Middle Eastern nations are actively re-evaluating their existing Middle East oil pipelines networks to sustain export capabilities. Three primary pipelines are currently under consideration as viable strategic alternatives to the Strait of Hormuz.

Saudi Arabia’s East-West Pipeline: A Robust Conduit

Operated by Saudi Aramco, the 1,200-kilometer East-West Pipeline, also known as Petroline, connects the Abqaiq oil processing center to the Red Sea port of Yanbu. This structural asset possesses a maximum capacity of 7 million barrels per day, with approximately 5 million barrels per day allocated for exports. Saudi Arabia has significantly amplified oil flow through this route since the conflict’s inception, demonstrating its strategic utility. However, this pipeline inherently depends on Red Sea shipping, including the Bab al-Mandeb Strait, a chokepoint vulnerable to potential disruption from Yemen’s Houthi movement.

UAE’s Abu Dhabi Crude Oil Pipeline: Direct Access to the Gulf of Oman

The Abu Dhabi Crude Oil Pipeline (ADCOP), or Habshan–Fujairah pipeline, extends 380 kilometers from Abu Dhabi’s oil fields to the port of Fujairah on the Gulf of Oman. Operational since 2012, this pipeline effectively transports around 1.5 million barrels per day. Recent data confirms an increase in exports from Fujairah, indicating Gulf producers are proactively seeking alternatives to the Strait of Hormuz to maintain consistent energy flow.

Iraq–Turkiye Crude Oil Pipeline: Northern Diversification

Connecting northern Iraq to Turkiye’s Mediterranean coast, the Iraq–Turkey pipeline (Kirkuk–Ceyhan pipeline) offers another vital alternative. Its design capacity reaches approximately 1.6 million barrels per day. Currently, flows are estimated at about 200,000 barrels per day. This pipeline represents a critical northern egress point for Iraqi oil, diversifying export pathways.

Evaluating Capacity: Limitations of Middle East Oil Pipelines as Full Replacements

Despite the inherent importance and strategic deployment of these pipelines, experts conclude they cannot fully compensate for a complete closure of the Strait of Hormuz. Collectively, the three primary routes can manage approximately 9 million barrels per day. This figure represents less than half of the 20 million barrels per day typically transported through the Strait, establishing a clear capacity deficit.

Furthermore, these pipeline infrastructures themselves remain vulnerable. The ongoing conflict poses a persistent threat of missile or drone strikes, a concern underscored by previous attacks on energy infrastructure across the Gulf region. Therefore, while offering partial solutions, these alternative routes introduce their own set of security challenges.

Logistical Constraints: Evaluating Other Alternatives for Oil Transportation

Other transportation modalities, such as trucking oil, face significant practical and economic barriers. A single truck typically transports a modest 100 to 700 barrels. Consequently, moving substantial volumes would necessitate thousands of vehicles, incurring prohibitive costs and presenting complex logistical challenges. As the conflict persists, analysts project that prolonged disruptions in the Strait of Hormuz will exert profound implications on global energy markets and fuel prices worldwide, underscoring the necessity for robust, long-term strategic energy solutions.

The Translation (Clear Context): Navigating Geopolitical Energy Dynamics

The current volatility around the Strait of Hormuz signifies a critical re-evaluation of global energy supply chain vulnerabilities. Iran’s actions to control transit translate to a direct assertion of regional power, converting a critical international maritime passage into a conditional route. This forces a recalibration of oil and gas flows, pushing Gulf states to activate contingency plans centered on existing pipeline infrastructure. The core logic is to maintain export stability by diversifying transport away from contested waters, though this introduces a new set of logistical and security considerations.

The Socio-Economic Impact: Calibrating Daily Life for Pakistanis

For the average Pakistani citizen, the Strait of Hormuz disruptions and the limitations of alternative Middle East oil pipelines have direct, tangible consequences. A reduction in global oil supply or increased transport costs due to longer routes translates directly to higher fuel prices at the pump. Consequently, this inflates transportation costs for goods, impacting food prices and general household budgets.

Students reliant on public transport for education and professionals commuting to urban centers will experience increased daily expenditures. Furthermore, industries dependent on stable energy supplies, such as manufacturing and agriculture, face operational uncertainties and higher input costs. This dynamic could affect job markets and overall economic stability, with rural Pakistan, often more sensitive to fuel price fluctuations, potentially experiencing disproportionately higher impacts.

The “Forward Path” (Opinion): Assessing Strategic Momentum

This development represents a Stabilization Move, rather than a definitive Momentum Shift. While the activation and increased utilization of Middle East oil pipelines are crucial for mitigating immediate supply shocks, they expose inherent limitations in capacity and security vulnerabilities. The global energy infrastructure remains precariously dependent on a few chokepoints, even with alternative routes. A true Momentum Shift towards energy resilience would necessitate greater diversification of energy sources, accelerated investment in renewable technologies, and more robust, multilateral security agreements protecting critical infrastructure across all modalities. Until then, these pipeline maneuvers serve as essential tactical responses to maintain equilibrium in a volatile geopolitical landscape.